Section 1231 Gain: Definitions, Examples, & Explanations

by Shahnawaz Alam Finance 21 July 2023

When someone is selling a business, they will probably face some capital gains or losses that have significant tax implications on the company.

Yes, businesses will probably gain some profits. But it is also possible to gain significant tax liabilities realized on the assets.

However, businesses can still reduce the tax burdens generated from capital gains. They can plan to dispose of depreciable business assets or real properties to reduce this tax burden. But planning is essential for this.

So, let’s learn about section 1231 gains through this article. I have listed the basic idea of section 1231 gains and how it works in this article.

What Is Section 2131 Gain?

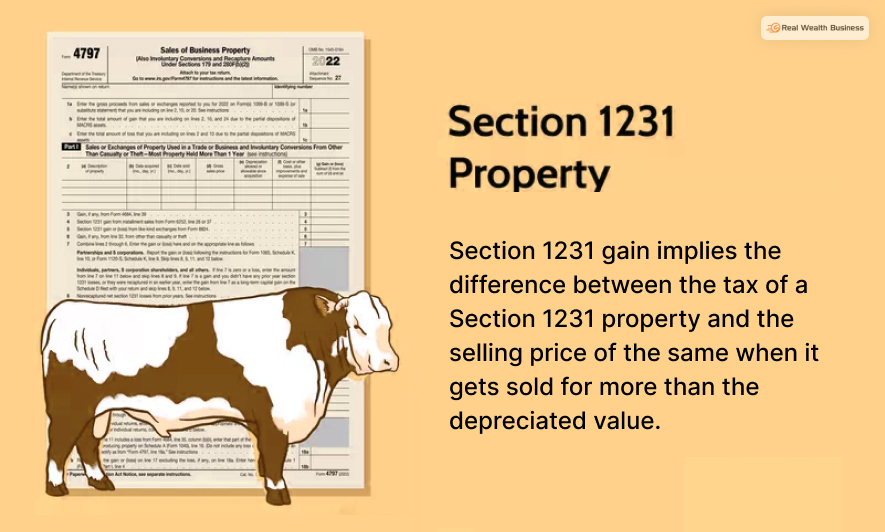

According to IRS, section 1231, assets are reals estate assets or real property that the company held for over a year. Section 1231 gain implies the difference between the tax of a Section 1231 property and the selling price of the same when it gets sold for more than the depreciated value. Compared to the ordinary gains rate, this amount is taxable at a very low gains rate.

So, how does an asset gain the capital gain treatment? For that, an asset has to be constructed or purchased for a business or for trade. Wait, that’s not all. The company also needs to hold the asset for more than a year. This tenure starts from the date of the asset’s purchase until it is sold. The company needs to qualify for tax treatment under Section 21.

So, what are some assets that qualify for Section 1231 gains? Here are some properties (used for business) that qualify under section 1231 – personal property, residential properties, commercial real estate, and different vacant lands, etc. Below, I have given more detailed examples of the same –

Different Types Of Section 1231 Transactions

Here is a list of assets that qualify for asset 1231 treatment –

- Buildings

- Vehicles

- Furniture

- Leaseholds

- Machinery & other equipment

- Rental Properties

- Unharvested crops

- Livestock purchased or resided for breeding, draft, dairy, or sporting.

There are other different properties that also qualify for selection 1231 treatment. For example, condemned properties or the ones impacted by theft can also qualify to get treated under section 1231. But this is only possible when the involuntary conversion causes any recognized gain.

A property is considered investment property when the owner can recoup their investment by selling any of such assets instead of using them.

The IRS regulation considers the following under section 1231 transactions. Go through this list to learn in detail about section 1231 transactions.

Thefts & Casualties

If a business or an owner holds property for more than a year and it gets adversely affected by theft, it can go under Section 1231 treatment. This adverse effect can also be caused by any other types of similar casualties.

Condemnation

When a property was held for over a year as a capital asset related to trade and business, it can be considered a Section 1231 transaction.

Sale Or Exchange Of Real Or Personal Depreciable Property

When a property was held for more than a year and was being used in business or trade, then it would come under section 1231 transactions. This usually applies to properties that were helping generate revenue through royalties or rents.

Leaseholds: Both Sold & Exchanged

Leaseholds also come under section 1231 transactions if they are used or traded or business or held for more than a year.

Animals Or Horses Exchanged Or Sold

When cattle are held for more than a year and are used for draft, dairy, breeding, or sporting games, they come under section 1231 transaction.

Unharvested Crops Sold/ Exchanged

Unharvested crops that are held for a year or more, or sold/exchanged or converted involuntarily, and then are not required – then they would come under section 1231 transaction.

Disposal Of Timber, Iron Ore, Coal, Etc

If these are treated as sales, then they would come under section 1231 transactions.

How To Calculate Section 1231 Gain?

It is pretty simple to calculate the section 1231 gains and losses. You Have to start by calculating the basis of the object. Here is the formula for that –

Purchase Price – Depreciation

Next, you have to subtract the basis price from the sale price of the item. If you are getting a positive result, then you have gains, but if the number is negative, then it means that you have incurred a loss.

Also, if the loss incurred due to condemnation, theft, or casualty, then your loss is equal to your basis.

Form 4562

So, you already know that you have to first determine the basis before calculating the loss or gain from your section 1231 properties. This suggests that you have to take depreciation into account. You can ensure that you have depreciated your assets properly; the IRS will have you file form 4562 alongside your yearly taxes that you claim depreciation. Both IRS and you can understand the amount of tax you have claimed on an asset.

Form 4797

You will need to file a form 4797 to calculate the basis of the asset. The IRS will require you to file a form 4797. This usually lists the properties you sold or lost, the purchase price, and the depreciation amount you claimed earlier. Then this information allows you to calculate your basis in the asset along with the gain and loss.

Tax Advantages Of Section 1231

Businesses gain tax advantages from Section 1231 from both gains and losses.

- Businesses gain long-term capital gains rates on different gains from assets and sales.

- Businesses can get their gains taxed at a lower rate for capital gains.

- But if the sold property was held for less than a year, the 1231 gain is not applicable.

Final Words

Yes, section 1231 is indeed a complex topic. But I made sure that you are learning something with ease after reading this article. However, while you are at it, you should also learn about 4562 and 4797. Once you understand how Section 1231 gains work, you will understand how to mitigate the tax burden generated from capital gains on different assets by planning ahead.

I hope that this article was helpful. Please let us know if you have any queries or confusion about the same.

Wait…before you leave, consider these top resources:

Related