What Is Bonus Depreciation? Definition And How It Works? – Let’s Find Out

by Shahnawaz Alam Finance Published on: 28 July 2023 Last Updated on: 07 November 2024

Many businesses struggle to pay their income taxes due to outstanding taxable income. However, some techniques like Bonus depreciation allow businesses to write off a large percentage of the purchase price.

As a result, entrepreneurs taking a step behind were more keen to purchase their assets and start a business. Bonus depreciation lowers the tax liabilities of a business.

But how does it work? What is bonus depreciation? If you are curious about bonus depreciation and determine which assets are qualified to claim this depreciation, then keep reading.

What Is Bonus Depreciation?

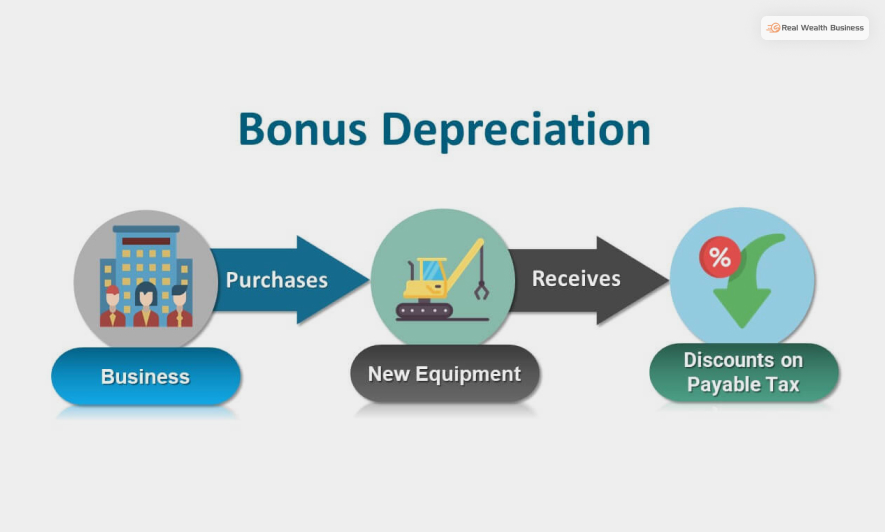

Companies sometimes have to pay a huge amount in income tax. They can reduce the payable amount for bonus depreciation thanks to Bonus depreciation. This tax incentive lets businesses deduct a massive percentage of the purchase cost of any eligible asset.

Instead of writing the cost off over the useful life cycle of the product, this depreciation process deducts a large percentage of the cost during the first year of its purchase.

This depreciation dates back to 2002 and was created by Congress’s Job Creation & Worker Assistance Act of 2002. The idea was to add it as a temporary deduction and encourage small firms to invest after the 9/11 attack.

Also, once a large portion of the asset is deducted, the remaining amount gets distributed throughout the years. However, the rules were changed again in 2017 by the Tax Cuts & Jobs Act. One of the major changes was the enactment of 100% bonus depreciation. This applied to the cost of acquired eligible assets and placed in service post-Sept. 27, 2017, & before 1st January 2023.

But, before TCJA, the Tax depreciation was 50%. The phase-out schedule is as follows –

- 2022 – 100%

- 2023 – 80%

- 2024 – 60%

- 2025 – 40%

- 2026 – 20%

- 2027 – 0%

How Does Bonus Depreciation Work?

Bonus depreciation is the process of purchasing specific and qualified business assets and then putting them into service before the year ends.

Next, the bonus depreciation gets reported to the IRS.

Here is an example for an even better understanding –

Let’s say that a business purchases a qualified asset in December of 2023. But they do not use the asset until January of 2023. In this case, if the business needs to wait, they file their tax return for 2023. Only when they file their tax returns for 2023 will they be ready to claim bonus depreciation on the software they purchased?

But, the asset a business claiming bonus insurance for should also be a qualified one. A businessperson is encouraged to start a business and add value to society through this depreciation technique. However, there is no rule of thumb for which businessman to opt for this depreciation technique.

Also, it is a special type of depreciation, and a business asset needs to pass through all the checklists to qualify. So, how does a business? Keep reading to find out.

Which Assets Qualify For Bonus Depreciation?

A business asset needs to meet specific criteria to qualify for bonus depreciation. Here are some checklists that your asset needs to pass –

- MACRS (Modified accelerated cost recovery system): properties that have a recovery period of less than 20 years. Computer equipment and office furniture are among such properties.

- Water utility property.

- Depreciable computer software.

- Qualified leasehold improvement property: this includes improvement to the interior portion of any nonresidential building. The improvement needs to be placed for more than three years after the first service date of the building.

- Cost of production for any film, TV, and live theatrical production.

- Vacation property also qualifies for bonus depreciation if the taxpayer is using it as a short-term rental property. If the short-term rental property is a commercial property, and if the taxpayer improves its interior, then it may qualify for bonus depreciation.

- The residential rental estate can also qualify for bonus depreciation. But only if the taxpayer is conducting a tax segregation study.

- Vehicles with a useful life of more than 20 years.

- Used equipment: if the taxpayer does not use the equipment anytime prior to the acquisition.

Which Assets Do Not Qualify For Bonus Depreciation?

The IRS disqualifies specific assets from claiming an amount in bonus depreciation. The bonus depreciation rules list certain assets that cannot qualify for bonus depreciation. Here is a list of those assets –

- Assets that were initially used in furnishing or selling electrical energy, sewage disposal service, water, etc.

- Assets initially used in furnishing trade or gas selling or steam-selling business through a distributed system.

- Assets initially used in furnishing trade or gas selling or steam-selling business via pipeline.

- Assets used in trade; or assets used in businesses that used to have floor plan financing indebtedness at any specific circumstances.

- Qualified improvement properties like leasehold improvements acquired after 31st December 2017 are also not qualified.

How To Calculate Bonus Depreciation?

Calculating bonus depreciation is not simple. Businesses need to multiply the bonus depreciation rate by the business asset’s cost. After that, deduct the property tax from the asset’s cost.

Here is an example –

- Let’s say that the cost of the asset is $1000000.

- The tax rate is 21%.

In that case, the bonus depreciation calculation would be as follows –

Bonus depreciation amount = cost of the asset $1000000 x 21%

The claimable bonus depreciation is = $210,000

So, if the cost of the asset is $1000000, then the depreciated value of the asset would be –

$1,000,000 – $210,000 = $790,000.

How To Report Bonus Depreciation?

Bonus depreciation gets reported on a federal tax return via Form 4562 (depreciation and amortization). This needs to be done by the due date of the federal tax return for the specific taxable year. The qualified property or assets needs to be placed in service for a taxable year by the taxpayer – which is why the taxable year here is “specific.”

Final Words

Thanks to the immediate deduction in the asset cost of eligible assets, businesses can use bonus depreciation as a tool for tax savings. This happens during the first year of the asset’s service. Thanks to bonus depreciation, a business can reduce its tax liabilities. Small businesses usually find this technique beneficial. If you own a small business and are purchasing assets qualified for this technique, then you can go for it.

However, we recommend doing more studies on bonus depreciation and how your assets and taxable income react to it. I hope that this article was helpful. Please let us know if you have any additional questions. We will try to solve them in due time. Thank you for reading.

Read Also:

Related