Comparison: Pure Term Plan & Term Plan with Return of Premium

by Abdul Aziz Mondal Insurance Published on: 01 April 2021 Last Updated on: 27 December 2024

The insurance sector in the country comes with a myriad of options for the citizens.

There are various insurance plans available that offer a ton of different coverage options for their customers.

These plans come with extensive features to help the policyholder during unfortunate events. Among the life insurance plans, there are three segments of insurance policies that are quite famous. They include- term plans, the return of premium term plans, and permanent life insurance.

These plans are separate in their unique ways. Let’s look at them individually to understand their differences better.

Pure Term Plan:

- It is a life insurance plan where the policyholder gets insurance coverage for a pre-determined term. If the policyholder survives the policy’s term, their policy ends. The Pure Term insurance policy only provides the death benefit and doesn’t provide any survival benefits.

- The coverage from this plan lasts for a specified term which can vary from 10 years up to 100 years of age.

- The plan offers flexible death benefit payouts – lumpsum or regular payout.

- If you surrender this plan before the policy’s tenure, your coverage will end there, and there will be no surrender benefits or payouts.

- As per Section 80C, the premiums paid for a pure term plan are eligible for a tax deduction. As per Section 80D, the critical illness rider’s premiums are eligible for a tax deduction. As per Section 10(10D), the death benefit paid is entirely tax-free.

- One of the most affordable forms of life insurance as the plan’s premiums is substantially low compared to other insurance plans. However, the premium amount goes up with age, so it is advisable to buy the policy at a younger age.

Term Plan with Return of Premium (TROP):

- The Term Plan with Return of Premium (TROP) is a type of insurance where the policyholder gets a life cover for a specified term. If they outlive the policy tenure, they will get the maturity/survival benefit.

- The survival benefit will include a sum of all the premiums paid during the policy term.

- The coverage with this plan lasts for a specified term which varies from 10 years up to 100 years of age.

- They are considered one of the best term insurance plans as they offer a death benefit as well as the return of the paid premium amount.

- If the policyholder surrenders the policy before the term, their cover will cease, and they get a small percent of the premiums paid towards the policy till the surrender date.

- As per Section 10(10D), the return on term insurance as death benefit collected through the plan is tax-free. Along with it, the survival payout received is also tax-free.

- As per Section 80D, the critical illness rider’s premiums are eligible for a tax deduction.

- As per Section 80C, the premiums paid are eligible for a tax deduction.

- Provides policyholders with the dual benefit of assured returns along with insurance coverage.

- Premiums are a bit higher than pure-term plans, but not high as in whole life policies.

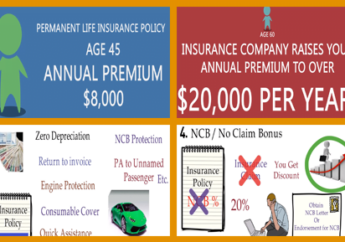

Permanent Life Insurance:

- It’s an insurance policy through which the policyholder gets the life cover for the entire life. Along with this, a part of the premium is deposited into non-market-linked avenues with guaranteed returns.

- The insurance coverage from the policy lasts for the policyholder’s entire life, as long as they keep paying the premium.

- The beneficiaries will get a fixed death benefit.

- The policyholder will get to benefit from the growing cash value.

- If you surrender the policy, the cover ceases, but the policyholder gets the interest earned on the investment component of the policy.

- As per Section 80D, the premium paid for the critical illness rider is eligible for a tax deduction.

- As per Section 80C, premiums paid are eligible for a tax deduction.

- As per Section 10(10D), the death benefits, as well as the maturity benefits, are completely exempt from taxation.

- It is a reliable form of life insurance. While the premiums are high, but they remain constant throughout the plan’s term.

Hence, as we understand, among the insurance policies available in the country, there are three main policies that the citizens generally prefer.

These three plans are different based on their features, and customers must understand their requirements before purchasing these plans.

Read Also:

Related