Bankruptcy Duration on Credit Reports: Answers from Resolvly Team

by Abdul Aziz Mondal Finance Published on: 29 June 2021 Last Updated on: 28 December 2024

When you’re faced with seemingly insurmountable debt, bankruptcy may seem like the only option you have left. As you prepare to take the plunge, you may find yourself asking common questions like, “How long does bankruptcy stay on my credit reports?” In this article, the Resolvly team answers this essential question.

We’ll discuss the unexpected pitfalls of filing for bankruptcy that many consumers overlook. We’ll also provide you with some viable alternatives that can leave you in a better financial situation. It may be possible to ditch that crippling debt and stay on the path to financial health at the same time!

Understanding the Impact of Bankruptcy

When they are unable to pay their debts, many consumers turn to bankruptcy to seek much-needed relief. While this is certainly an option, bankruptcy is not something that should be taken lightly.

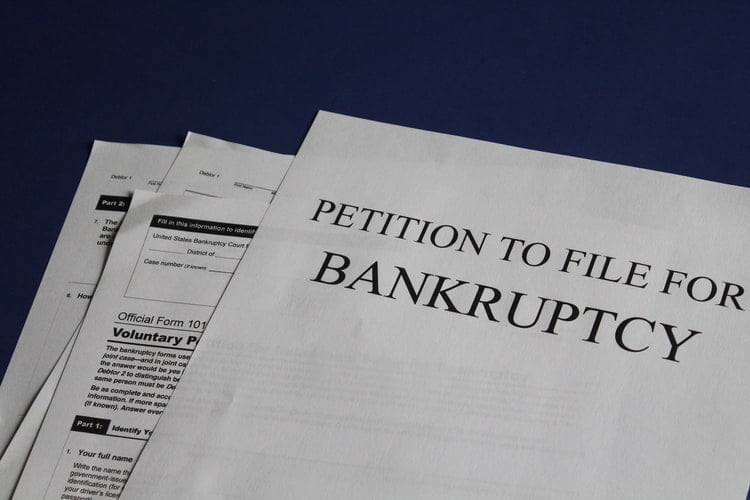

Contrary to popular belief, filing for bankruptcy does not immediately give you a clean slate. Bankruptcy will ruin your credit for years to come.

Generally, a bankruptcy filing will remain on your credit reports for seven to ten years. This major blemish will make it difficult to:

- Buy a home

- Obtain lines of credit

- Get approved for personal loans with good rates

- Purchase a vehicle

Remember, filing for bankruptcy is supposed to be an opportunity to start over. Imagine how hard that could be if you cannot get a reasonable interest rate on a car loan. There may come a time at which bankruptcy truly is the best option to address your debt. However, far too many consumers file for bankruptcy when there are better solutions on the table.

Additional Concerns

In addition to the potential impact on your credit score, filing for bankruptcy presents a few other problems. If you file for Chapter 7 bankruptcy, you will have to sell off any asset that is not considered exempt. The money from this sale will be used to pay off your creditors.

One alternative type of bankruptcy is known as Chapter 13 bankruptcy. This process allows you to keep your belongings. However, you will have to repay at least part of your debt. When you file for Chapter 13 bankruptcy, the court will implement a repayment plan that covers a period of three to five years.

Regardless of which type of bankruptcy you file for, certain types of debt may not be addressed at all. For example, a Chapter 7 bankruptcy does not excuse any overdue taxes or student loans.

What Are the Alternatives to Bankruptcy?

As you can see, there are multiple drawbacks to filing for bankruptcy. For most consumers, it’s a much more practical solution to negotiate settlements, balance reductions, or even complete debt dismissal.

Understanding your rights as a consumer and negotiating with collection agencies can be quite challenging. If you want to ensure that your rights are protected, you will need to partner with an experienced debt resolution attorney.

Resolvly can connect you with a consumer law attorney in your state to get the process started. They will help you pursue financial freedom and seek favorable debt resolution terms.

Read Also:

Related