Strategic Financial Planning for Growing Small Businesses

by Barsha Bhattacharya Blog 09 March 2026

Growing a small business often needs wise financial choices. Finding the right money can make all the difference. Small Business Administration (SBA) loans are a key tool for many entrepreneurs in the U.S. These government-backed loans help businesses start, grow, and succeed.

In this guide, we will explore what SBA loans are and how they work. We will look at the different types of loans available and who can get them. We will also cover the application process and common mistakes to avoid.

Whether you are buying a new building or need cash to run your daily business, understanding SBA small business financing can help you reach your goals. We will also touch on similar options for our Canadian neighbors.

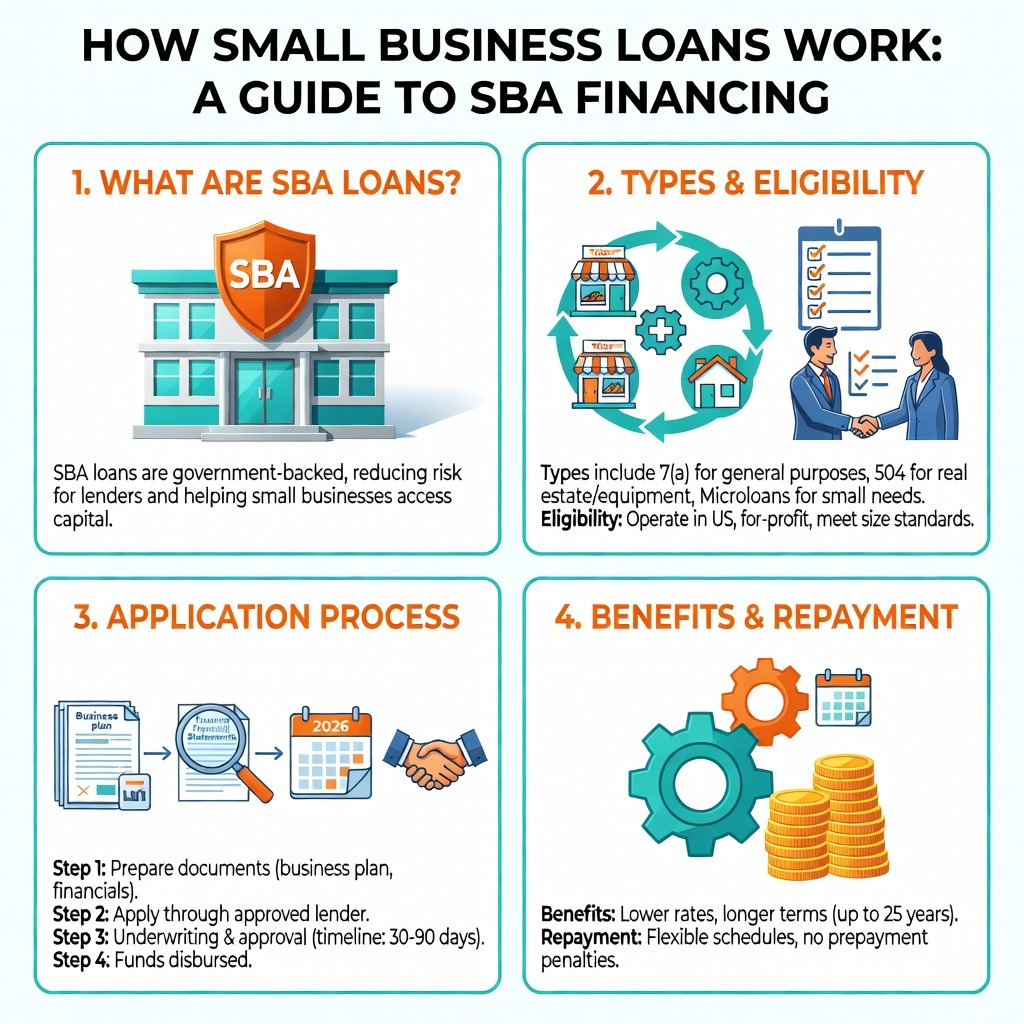

At its core, small business financing, particularly through programs like those offered by the U.S. Small Business Administration (SBA), aims to bridge the gap between traditional lending and the unique needs of small businesses. Unlike conventional loans, which banks issue directly and bear full risk, SBA loans involve a government guarantee. This guarantee reduces lenders’ risk, making them more willing to approve loans for businesses that might not qualify for conventional financing due to limited collateral, shorter operating history, or other factors.

SBA loans are not issued directly by the SBA. Instead, they are provided by banks, credit unions, and other financial institutions, with the SBA guaranteeing a portion of the loan. This structure allows small businesses to access capital with more favorable terms, including lower down payments, longer repayment periods, and competitive interest rates, than they might otherwise obtain.

The SBA offers several core loan programs, each designed to meet different business needs:

- 7(a) Loan Program: This is the SBA’s primary program, offering flexible financing for a wide range of general business purposes. It’s highly adaptable, covering everything from working capital to real estate acquisition. The maximum loan amount for a 7(a) loan is $5 million. The SBA guarantees up to 85% of loans of $150,000 or less, and up to 75% of loans above $150,000.

- 504 Loan Program: This program provides long-term, fixed-rate financing for significant fixed assets, such as real estate or heavy equipment. It typically involves a partnership between a commercial lender, a Certified Development Company (CDC), and the borrower. The SBA portion of a 504 loan can go up to $5.5 million.

- Microloan Program: Designed for tiny businesses and startups, these loans provide up to $50,000. They are often used for working capital, inventory, or equipment. SBA Microloans have an average loan size of about $13,000.

Here’s a quick comparison of these key SBA loan types:

Loan Type Maximum Amount Typical Uses Repayment Terms (Max) Key Feature 7(a) $5 million Working capital, equipment, real estate, acquisitions 25 years (real estate) Most flexible, general purpose 504 $5.5 million Fixed assets (real estate, equipment) 25 years (real estate) Long-term, fixed-rate for significant assets Microloan $50,000 Working capital, inventory, equipment, supplies 6 years Small loans for startups and tiny businesses Finding the Right Small Business Financing Lenders

Securing an SBA loan begins with finding an approved lender. The SBA itself does not lend money directly, except in disaster situations. Instead, it works with a vast network of banks, credit unions, and other financial institutions that process and disburse the loans.

To simplify this search, the SBA offers a valuable tool called Lender Match. This online platform connects small businesses with more than 800 SBA-approved lenders nationwide. By answering a few questions about your company and its needs, you can receive an email with potential lenders within two days. This allows you to compare rates and terms from interested lenders and choose the best fit for your specific situation. Additionally, local district offices and SBA resource partners, such as SCORE, Small Business Development Centers (SBDCs), and Women’s Business Centers, can provide guidance and help you navigate the process.

Choosing the Best Small Business Financing for Your Needs

The best SBA loan for your business depends entirely on your specific financial goals.

- Working Capital: If you need funds for day-to-day operations, inventory, or cash flow management, a 7(a) loan or a Microloan (for smaller amounts) would be suitable.

- Buying Equipment: For purchasing machinery, vehicles, or other tangible assets, both 7(a) and 504 loans are excellent options. The 504 program is ideal for large, long-term equipment purchases because of its fixed-rate structure.

- Real Estate: Acquiring or renovating commercial property is an everyday use for both 7(a) and 504 loans, with 504 often preferred for its fixed-rate, long-term nature for real estate. SBA 7(a) loans can have maturity terms up to 25 years for real estate.

- Debt Refinancing: The 7(a) program can also be used to refinance existing business debt under certain conditions, potentially improving cash flow with better terms.

- Business Expansion or Acquisition: For purchasing an existing business or funding significant growth initiatives, a 7(a) loan is often the go-to choice due to its flexibility.

Carefully assessing your needs and understanding the features of each loan type will guide you toward the most appropriate SBA funding solution.

How to Qualify for SBA Funding Programs

Eligibility for SBA loans is a crucial first step. While specific requirements can vary slightly between programs and lenders, several general criteria apply to most SBA loans.

To be eligible, a business must typically:

- Be an operating business: The business must be actively engaged in trade or commerce.

- Operate for profit: Non-profit organizations are generally not eligible for standard SBA loan programs.

- Be located in the U.S.: The business must primarily conduct its operations within the United States.

- Be small under SBA size standards: The SBA defines “small” based on industry-specific revenue thresholds or employee counts. These standards ensure that the loans benefit genuinely small enterprises.

- Not be a type of ineligible business: Certain industries are excluded, such as those involved in speculation, gambling, or passive investment.

- Be unable to obtain the desired credit on reasonable terms from non-federal, non-state, and non-local government sources: This “credit elsewhere” test ensures that SBA loans serve businesses that genuinely need the government guarantee to secure financing.

- Be creditworthy and demonstrate a reasonable ability to repay the loan: Lenders will assess your personal and business credit history, cash flow, and financial projections. Even companies with bad credit may qualify for startup funding under some SBA programs, though stronger credit profiles typically secure better terms.

- Have a sound business purpose: The loan proceeds must be used for legitimate business expenses that align with the program’s objectives.

Meeting the Equity Injection Rules

For many SBA loans, particularly those for business acquisitions or startups, an equity injection or down payment is a critical requirement. While the exact percentage can vary, a standard expectation is around 10% of the project cost. This injection demonstrates the borrower’s commitment and reduces the lender’s risk.

The equity injection doesn’t always have to be 100% cash. It can come from various sources:

- Cash Savings: The most straightforward form, using liquid funds from the borrower. Lenders often prefer at least half of the equity injection to be in cash.

- Seller Notes: In business acquisitions, a portion of the purchase price can be financed by the seller, often structured as a “seller note on standby.” This means the seller agrees to defer payment until the SBA loan is repaid, effectively acting as equity.

- Owner Investment: This can include capital contributions from the business owners or investors.

- Other Assets: In some cases, certain business assets or equipment may count toward the equity injection, provided they are appropriately valued and meet SBA guidelines.

Understanding and planning for this equity injection is vital for a successful application.

Exceptional Help for Disaster Recovery

Beyond its standard lending programs, the SBA plays a crucial role in helping businesses and homeowners recover from declared disasters. SBA Disaster Loans are direct loans from the SBA that offer low-interest, long-term financing to repair or replace damaged property, inventory, and other business assets.

In disaster recovery situations, the SBA is committed to supporting survivors in rebuilding homes and businesses as quickly as possible. To expedite this, new options have been introduced to bypass permitting delays. For instance, if you applied for a local permit more than 60 days ago without approval, you may qualify for a self-certification option. This initiative helps businesses and individuals move forward with rebuilding efforts more swiftly, reducing the burden of bureaucratic hurdles during already challenging times.

Comparing SBA Loans to Conventional Options

When seeking business financing, entrepreneurs often weigh SBA loans against conventional bank loans. While both provide capital, they differ significantly in their structures, eligibility criteria, and terms.

How SBA Loans Differ from Conventional Business Loans:

- Government Guarantee: The most significant difference is the SBA’s guarantee, which mitigates lenders’ risk. This makes SBA loans more accessible to startups or businesses with less-established credit histories or limited collateral. Conventional loans carry 100% of the risk for the lender.

- Eligibility: SBA loans are designed specifically for small businesses that might struggle to get conventional financing on reasonable terms. Conventional loans typically require stronger credit, longer operating histories, and substantial collateral.

- Down Payments: SBA loans often require lower down payments (e.g., 10% for acquisitions) than conventional loans, which may require 20-30% or more.

- Repayment Terms: SBA loans generally offer longer repayment terms, resulting in lower monthly payments and improved cash flow. For instance, real estate loans can have terms of up to 25 years, while equipment and working capital loans can have terms of up to 10 years. Conventional loans usually have shorter terms, often 5-7 years for equipment and even less for working capital.

- Interest Rates: While conventional loans can sometimes offer slightly lower rates for highly qualified borrowers, SBA loan rates are competitive and capped by the SBA, tied to the prime rate. This protects excessively high rates.

- Collateral: While collateral is usually required for SBA loans, the SBA’s guarantee can make lenders more flexible when a business has insufficient collateral. Conventional loans often demand significant collateral.

- No Balloon Payments: SBA loans are fully amortized, meaning they are paid off entirely by the end of the term, with no large “balloon” payment due at the end. This provides greater financial predictability.

Benefits for Business Acquisitions

SBA loans are particularly advantageous for business acquisitions. When purchasing an existing business, a significant portion of the value often lies in “goodwill” or intangible assets, which traditional lenders are hesitant to finance. SBA loans, especially the 7(a) program, are more amenable to funding of these intangible assets.

The longer repayment terms offered by SBA loans also make acquisitions more manageable. A 10-year term for an acquisition loan can significantly reduce monthly payments compared to a conventional 5-year term, allowing the new owner to preserve cash flow for operations, integration, and growth. This flexibility can be crucial for the long-term success of the acquired business.

Drawbacks to Consider

Despite their many benefits, SBA loans also come with certain drawbacks that borrowers should be aware of:

- Application Process: The SBA loan application process can be more extensive and time-consuming than that for conventional loans. It often involves more paperwork and a longer approval timeline because it must satisfy both the lender’s and the SBA’s requirements.

- Fees: SBA loans include an upfront guaranty fee and an annual service fee, both paid to the SBA. These fees are typically a percentage of the guaranteed portion of the loan and can add to the overall cost, though they can often be financed into the loan.

- Collateral and Personal Guarantees: While the SBA guarantee reduces lender risk, borrowers are still typically required to provide collateral and, often, a personal guarantee from owners with 20% or more ownership. This means personal assets could be at risk if the business defaults.

- Prepayment Penalties: For some SBA loans, particularly larger 7(a) loans with maturity terms of 15 years or more, prepayment penalties may apply if a significant portion of the loan is paid off early within the first few years. Specifically, penalties are 5% in year 1, 3% in year 2, and 1% in year 3, for prepayments of 25% or more.

- Strict Use of Funds: Loan proceeds must be used for approved business purposes, with less flexibility than some conventional financing options.

Understanding these potential drawbacks is essential for a comprehensive financial strategy.

International Alternatives and the Canadian Market

It’s important to clarify that “Small Business Administration loans” (SBA loans) are specific to the United States. The SBA is a U.S. government agency, and its programs are not available in other countries. However, many nations offer similar government-backed financing programs to support their small and medium-sized enterprises (SMEs).

For our Canadian neighbors, the primary equivalent to the U.S. SBA loan programs is the Canada Small Business Financing Program (CSBFP). This program, administered by Innovation, Science and Economic Development Canada, helps small businesses obtain loans from financial institutions by sharing the risk with lenders. Over the past 10 years, small businesses have received more than 53,000 CSBFP loans totalling more than $11 billion, underscoring the program’s significant impact.

The CSBFP offers:

- Term Loans: Up to $1,000,000 for purchasing or improving land, buildings, equipment, or leasehold improvements.

- Lines of Credit: Up to $150,000 for working capital.

- Maximum per Borrower: A total maximum of $1.15 million per borrower ($1,000,000 term loans + $150,000 lines of credit).

- Government Guarantee: The government guarantees 85% of the loan amount, thereby reducing lenders’ risk.

- Registration Fee: A 2% one-time registration fee is applied to the loan amount and can often be financed into the loan.

- Interest Rates: Rates are typically floating (Prime + up to 3%) or fixed (mortgage rate + up to 3%), with lines of credit at Prime + up to 5%.

How the CSBFP Helps Canadian Owners

The CSBFP is designed to make it easier for small businesses in Canada to access the capital they need to start, grow, and modernize. It addresses the challenges that many small businesses face in securing conventional financing.

Funds from the CSBFP can be used for a variety of purposes:

- Working Capital: To cover day-to-day operational expenses, inventory, or cash flow management.

- Leasehold Improvements: Renovating or fitting out leased business premises.

- Equipment: Purchasing new or used equipment, machinery, or commercial vehicles.

- Building Purchase/Improvements: Acquiring or renovating commercial real estate.

- Intangible Assets: Financing costs associated with intellectual property, franchise fees, or other intangible assets.

To be eligible, a business must generally be a small business or start-up operating in Canada with gross annual revenues of $10 million or less. Farming businesses are not eligible for this program, but they are eligible for a similar program under the Canadian Agricultural Loans Act.

Other Canadian Resources

In addition to the CSBFP, Canadian entrepreneurs have access to several other valuable resources and financing programs:

- Business Development Bank of Canada (BDC): A federal Crown corporation that provides financing, advisory services, and capital to Canadian businesses, with a focus on innovation and growth. BDC often fills gaps left by traditional banks.

- Futurpreneur Canada: Offers financing, mentoring, and support to young entrepreneurs (18-39) launching or acquiring a business.

- Canadian Agricultural Loans Act Program: A federal program specifically designed to help farmers and agricultural co-operatives get loans to establish, improve, and develop farms.

- Provincial and Territorial Programs: Many provinces and territories also offer their own business support and financing initiatives.

To explore a comprehensive list of federal, provincial, and territorial programs and services that match your business needs, the Canada Business Benefits Finder is an excellent resource.

Navigating the Application Process and Avoiding Mistakes

The application process for an SBA loan, while thorough, is manageable with proper preparation. It typically involves several key steps:

- Determine Eligibility: Ensure your business meets the general SBA and specific program requirements.

- Prepare a Strong Business Plan: This document is crucial for demonstrating your business’s viability, conducting market analysis, outlining your management team, and providing financial projections.

- Gather Financial Documents: Collect personal and business financial statements, tax returns, bank statements, and any existing debt schedules.

- Find an SBA-Approved Lender: Use tools like SBA Lender Match or contact local banks and credit unions.

- Submit Application: Work with your chosen lender to complete their specific application forms and submit all required documentation.

- Underwriting and Approval: The lender reviews your application, performs due diligence, and seeks the SBA guarantee.

- Closing: Once approved, you’ll sign the loan documents, and the funds will be disbursed.

Common Mistakes to Avoid

Applying for an SBA loan can be complex, and inevitable missteps can delay or even derail your application. Here are common mistakes to avoid:

- Incomplete or Inaccurate Documentation: This is one of the most frequent causes of delays. Ensure all required documents are meticulously prepared, accurate, and up to date. Missing information or discrepancies can lead to significant setbacks.

- Weak Business Plan: A poorly constructed business plan that fails to clearly articulate your business model, market opportunity, management capabilities, and financial projections will raise red flags for lenders.

- Poor Credit History: While SBA loans are more forgiving than conventional loans, a very low credit score or recent bankruptcies can still be a significant hurdle. Work to improve your credit before applying if possible.

- Unrealistic Financial Projections: Overly optimistic or unsupported financial forecasts can undermine your credibility. Lenders want to see realistic, well-researched projections that demonstrate your ability to repay the loan.

- Lack of Equity Injection: Failing to demonstrate sufficient personal investment or equity in the business (e.g., the 10% down payment) can signal a lack of commitment.

- Applying to the Wrong Lender: Not all SBA-approved lenders are the same. Some specialize in certain loan types, industries, or loan sizes. Researching and choosing a lender that aligns with your specific needs can streamline the process.

- Not Understanding Loan Terms: Failing to grasp the interest rates, fees, repayment schedule, and any covenants can lead to future financial difficulties. Read all terms and conditions carefully.

- Lack of Collateral or Personal Guarantee: While the SBA guarantees a portion, lenders will still require collateral and often a personal guarantee, especially for owners with significant equity. Not being prepared for this can be a deal-breaker.

Understanding Fees and Penalties

SBA loans, like most financial products, come with associated costs. Being aware of these up front is crucial for accurate financial planning.

- SBA Guaranty Fees: These are paid by the lender to the SBA but are often passed on to the borrower. They are typically based on the loan amount and the guaranteed portion. For example, for a 7(a) loan, the fee might be 3.5% on the guaranteed portion up to $1 million and 3.75% on amounts over $1 million.

- Annual Service Fee: An ongoing fee paid to the SBA, usually a small percentage (e.g., 0.55%) of the outstanding guaranteed balance.

- Lender Fees: Lenders may charge their own fees, such as application, packaging, or closing costs. These should be transparently disclosed. Total closing costs for an SBA loan can range from 2% to 6% of the total project cost, covering items such as legal fees, appraisals, and environmental reports.

- Prepayment Penalties: As mentioned earlier, prepayment penalties can apply to 7(a) loans with maturity terms of 15 years or longer if more than 25% of the outstanding principal is prepaid within the first three years. These penalties are 5% in year one, 3% in year two, and 1% in year three. Most working capital or equipment loans with terms of 10 years or less typically do not have prepayment penalties.

Always discuss all potential fees and penalties with your lender during the application process to avoid any surprises.

Frequently Asked Questions about SBA Loans

What is the maximum amount I can borrow?

The maximum loan amount varies significantly by program. For the most common program, the SBA 7(a) loan, the maximum is $5 million. If you’re looking for smaller funding to get started or for specific needs, SBA Microloans cap out at $50,000, with an average loan size of about $13,000. For Canadian businesses under the CSBFP, the maximum is $1.15 million ($1,000,000 for term loans and $150,000 for lines of credit).

Can I use the money to buy a building?

Yes, absolutely. One of the most popular uses for SBA loans is the purchase or renovation of commercial real estate. Both the 7(a) and 504 loan programs are excellent options for this purpose. The 7(a) program offers flexible terms, while the 504 program is designed explicitly for significant fixed assets like real estate, offering long-term, fixed-rate financing. SBA 7(a) loans can have maturity terms up to 25 years for real estate, providing ample time for repayment and helping to manage cash flow.

Do I need a perfect credit score?

While a strong credit score (typically 680 or higher) will undoubtedly improve your chances and potentially secure better terms, a “perfect” credit score is not always required for an SBA loan. The SBA’s mission is to help small businesses that might not qualify for conventional financing. Lenders evaluate your creditworthiness holistically, including your business plan, cash flow projections, industry experience, and character. For startups or those with less-than-perfect credit, especially with Microloans, demonstrating strong repayment ability and a sound business purpose can be more critical than a pristine credit history. Collateral and a solid business plan can also help mitigate risk for the lender.

Conclusion

Navigating the landscape of small-business financing can seem daunting, but with the proper knowledge and strategic planning, it becomes a powerful tool for growth. SBA loans, with their government guarantee and favorable terms, offer a lifeline to many entrepreneurs who might otherwise struggle to secure capital. From the flexible 7(a) loans to the asset-focused 504 program and the accessible Microloans, there’s a solution tailored for various business needs.

Understanding eligibility, preparing thoroughly for the application process, and being aware of potential fees and pitfalls are critical steps toward success. And for our Canadian counterparts, robust programs like the CSBFP provide similar opportunities for growth and stability. By embracing thoughtful financial planning and leveraging these valuable resources, small businesses can confidently pursue their funding goals, expand their operations, and build a foundation for lasting success.

Related