What is a Fiduciary | Is Someone Else Calling the Shots?

by Ankita Tripathy Finance 06 November 2024

Yes, that is a common misconception that we hear all the time. If you are wondering what is a fiduciary and how it all works (don’t worry, no one else is forcibly responsible for what’s yours.) A fiduciary can be a person or an organization who acts on behalf of others. They cater to their client’s needs and interests ahead of their own.

Fiduciaries are not someone’s legal guardian – that’s another domain of responsibility. They are primarily involved in managing finances and may even cater to the well-being of another individual. Fiduciaries usually take care of their client’s financial assets.

From managing to advising, they can play various roles based on the discussions with their clients. They are also in a legally binding contract that puts the client’s interests at the center.

Let’s explore the meaning of the term and the various aspects of this responsibility from a wealth management perspective.

What is a Fiduciary | Fiduciary Definition, Their Responsibilities?

Various business relationships involve fiduciary duties, and they are applicable in multiple contexts, from shareholders to board members and beneficiaries. Fiduciary duties appear in relationships such as trustees and those receiving the legacy.

Much like the legal guardian of a child, house, or business, an investment fiduciary can be anyone legally responsible for someone else’s money. It is essential when considering all your efforts to build wealth and ensure your future generations have assets to rely on.

Introduced recently by the Department of Labor, fiduciary introduces transparency between the client and financial advisors. The clients must receive the best advice as investors, not advice that will benefit the advisor.

Responsibility & Relevance in Today’s Time

It is an essential barrier to fraud that has been prominent recently when investors have run into conflicts of interest. A vast variety of business relationships define what is a fiduciary from lawyers and clients to executors and beneficiaries.

The fiduciary responsibility is to steer clear of any conflicts of interest by operating transparently and holding themselves to a high standard of trust. Their role is to assist their client without thinking of personal gain and performing their duties with care.

Their role is to fully disclose to their client and present the services they were charged for. Broker-dealers may have a less strict standard per the SEC regulation implemented in 20119.

Fiduciary responsibilities are mainly financial, where they act in the party’s best interest instead of their own. It is an ethical and legal relationship between the service provider and the client built on trust between the parties.

A fiduciary duty involves actions taken in the client’s best interest – from duty of care, prudence, and confidentiality. Even the corporate workplace you’re in has a fiduciary responsibility towards you.

The fiduciary legally owns the property and controls the assets in their relationship. So yes, to answer the titular question, someone else is calling the shots.

But it is not by keeping you in the dark and not giving you any idea whatsoever of the decisions – there is comprehensive estate planning that goes in.

Let us look at the different examples of fiduciaries to know this concept better.

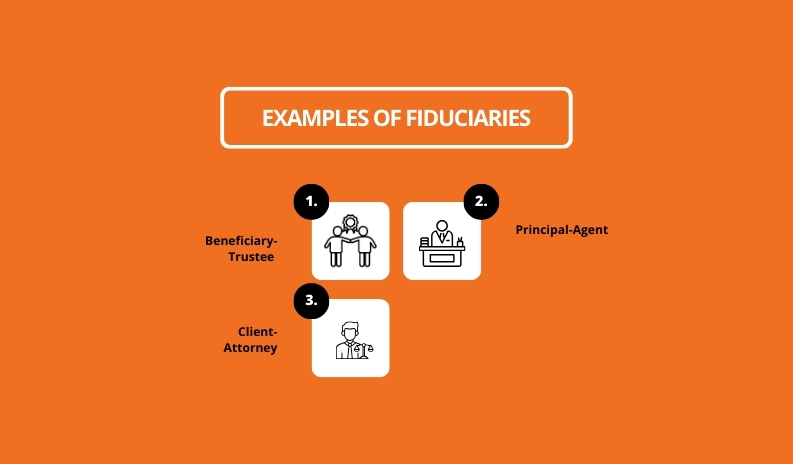

Examples of Fiduciaries

Fiduciary is mainly in wealth management, where the trustee legally takes responsibility for the client’s assets. However, there can be variations of this responsibility, and they are:

Beneficiary-Trustee

Take this example: an individual has created a living trust that their children will inherit should they pass away while the child is still underage. The parent shall then name an entity or a person to manage the trust.

It can be a bank, law firm, or a third party who has a fiduciary duty to the child/children. The legal ownership of the living trust and the property will be with the trustee in the trustee-beneficiary relationship.

The trustee must make decisions in the beneficiary’s best interest, who has equal title to the property/trust. One of the essential parts of asset protection planning is that the fiduciary, in this case, will take special care.

Thus, if you are thinking of starting a living trust for your child, be careful in determining who will be the trustee.

Principal-Agent

Any corporation, partnership, or government agency may act as an agent on behalf of a principal without any conflict of interest. A classic example of this relationship is the fiduciary duty of the executives and the shareholders.

The shareholders expect executives to make prudent decisions that are well-thought-of and are in the best interest of the owners (shareholders.)

Similarly, if you have a fund manager, you and they have a similar fiduciary relationship.

Client-Attorney

One of the most stringent fiduciary relationships requires the highest confidence and trust between a client and an attorney. The role of an attorney as a fiduciary is to act in all fairness, legality, and care on behalf of the client.

If you find your attorney to breach their fiduciary duties, you can hold them accountable in a court of law.

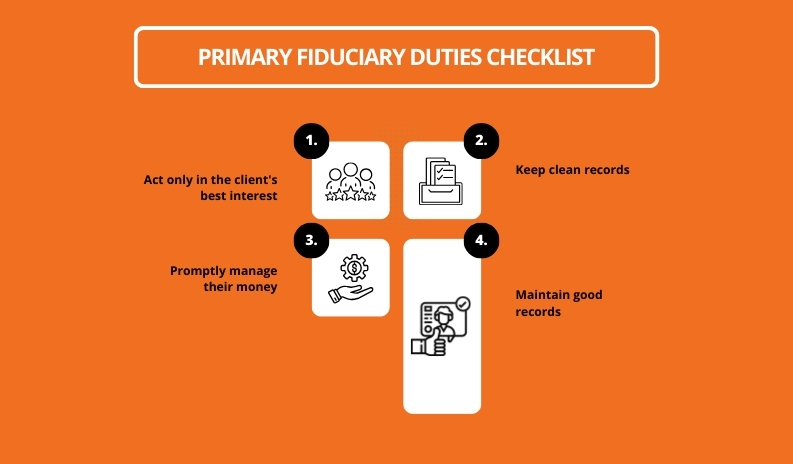

These were the basic examples illustrating what a fiduciary is and their different roles. There are four essential duties of the fiduciary apart from being transparent.

Primary Fiduciary Duties Checklist

So far, you may have understood the essential role of the fiduciary. They are simply a part of your basic duties in the industry. These are:

- Act only in the client’s best interest: When you have a fiduciary duty towards someone, you are legally bound to think in their best interest. It is unacceptable on several grounds for you to act in your best interest instead of the client.

- Keep clean records: this is important to keep your client away from legal problems. As the fiduciary, it is necessary to not mix their property or money with your own or someone else’s. Failing to do so will result in trouble with the IRA or the police and other government agencies.

- Promptly manage their money: The most important duty for you as a fiduciary is to carefully carry out your financial responsibilities. Overseeing their bank accounts, paying the bills, any unpaid debts, and taxes, and making investments on their behalf. As their fiduciary, you are also responsible for getting any insurance for the client as necessary.

- Maintain good records: Complete records of the assets will help you avoid legal consequences and ensure no gaps in your work. Keeping complete records will help you ensure that the services are in line with your financial needs.

What is a Fiduciary Bond? | Financial Advisor Vs Fiduciary & 2 Essential Considerations

If you were wondering what is a fiduciary bond, it involves insurance that is mandatory by the court to protect the financial well-being of the beneficiaries. It guarantees that the fiduciary will take care of the client’s financial well-being.

This is by state law, which requires fiduciaries to carry out their duties ethically and legally. Consider the agreement binding the fiduciary to the financial responsibilities per the client’s needs.

Many confuse a fiduciary bond with a fiduciary deed. When, indeed, they are different. The fiduciary deed is one of the several types involved in property transfers. For example, if your parent has a property but cannot sign it legally or for a different reason, this deed will be helpful.

Fiduciary deeds help in settling estates when the original owner is unavailable. It may be a fiduciary ownership or asset handling in the name of trust. In many cases, when not otherwise appointed – the trustee is the fiduciary.

Financial Advisor Vs. Fiduciary

Another obvious question we often get asked is whether a financial advisor is the same as a fiduciary. They are not unless they are appointed to be the fiduciary. As a financial advisor, it is the role of the advisor to be truthful in their guidance to the client.

Failing to do so can result in legal consequences for them. However, advisors are not managing the assets on behalf of the client – they simply advise. They also recommend based on what suits the client rather than picking the best option.

On the other hand, a financial fiduciary will take care of the client’s needs to the best of their ability and keep their interests ahead of their own. Often, fiduciaries are paid in a way that aligns with the incentives, whereas advisors may come at a flat fee.

So, if you are wondering if you require a financial advisor or a fiduciary, here are the top two considerations:

- If you require unbiased advice for big decisions about your financial security – go to a financial advisor.

- You need someone who will keep your gains before theirs – advisors will seldom do that – and that’s a slim chance. Opt for a fiduciary who will stick to the fiduciary standards.

Common Breach of Fiduciary

It hardly occurs, but these are some of the common breaches of fiduciary breaches you should keep in mind:

- Misinterpretation: This is a common issue when dealing with financial advisors, where they make false statements about a security transaction. This can be a gross fiduciary breach that can attract legal consequences for the advisors.

- Account churning: Another breach that applies when there is an excessive number of trades.

- Make unauthorized trades: This is significant as a financial advisor managing a client’s assets – do not forget to ask for the client’s approval before trading. Unless the situation involves a dead client with an underage heir, you should follow protocol.

- Negligence: Negligence on the advisor’s or fiduciary’s part harms the client. In addition, this involves any other breach outside those mentioned above.

If you are the fiduciary, you can avoid these breaches by adhering to the fiduciary standards and keeping your client on the same page as you. The management of a client’s property or assets is legally up to your organization, or you when you are the fiduciary.

Wrapping It Up!

That was all about what a fiduciary is and everything you need to know about the concept. This is from the perspective of a new business owner looking to take care of their assets in the long run.

It is also an essential part of wealth management and planning for future generations in the best way possible. In addition, it is also vital that you, as a client, know which service to opt for when looking to manage your wealth.

Lastly, it is essential that you keep in mind all the breaches that may occur; this is relevant from both ends as it prevents legal consequences.

Additional Reading: